Guest Article by Ian Cookson

If 2008 can be characterized as a year in which private equity buyers battled to acquire aircraft component manufacturers, then 2009 was a time of strategic acquirers fighting to secure defense technologies.

2009 was a relatively strong year for mergers and acquisitions. Defense technology saw a 6% increase in M&A activity in 2009 with a particularly strong second half of the year. This contrasts with M&A activity as a whole, which showed a 9% decline in the number of U.S. transactions across all sectors. M&A activity is likely to continue as the DoD, shaped by the 2010 QDR, shifts away from “big iron” and focuses on high-demand, low density assets such as unmanned aircraft, cyber security, and Command, Control, Communication, intelligence, Surveillance and Reconnaissance (C3ISR) technology. Defense contractors and government IT providers, mirroring these shifts in spending priorities, are actively looking to acquisitions to enhance their capabilities. Earnings for our defense IT company index rose 8% (EBITDA) during the year, and defense electronics company earnings rose 5%…

Prime defense and government IT contractors seek growth in defense technology

(click to view full)

There has been continued competition among prime defense contractors, traditional government IT providers and private equity players for strategic acquisitions within the defense technology sector. Acquirers are building capabilities in market niches within homeland security, cyber security, logistics support, navigation and guidance, and interactive training and simulation, among others.

Private equity has sought out opportunities with buyers coming from 2 camps – those traditionally focused on technology, and those with a defense specialty. Over the past 12 months, half of sponsor-led deals were bolt-on acquisitions that added expertise and capabilities to current portfolio companies, while half were new platform investments. Recent private equity successes such as the sale of BBNT to Raytheon are likely to attract attention and increase future investments.

Smaller businesses were the focus of attention, as transactions with values less than $100 million accounted for 90% of acquisitions. The cyber and homeland security segments were of particular interest, accounting for more than 40% of deal volume over the last year, as buyers took advantage of accelerated spending aimed at protecting against cyber and terrorist attacks.

(click to view full)

Prime defense contractors (e.g., Raytheon, Lockheed Martin, Northrop and Boeing) are especially interested in acquisitions that can be incorporated into current offerings to create fully integrated intelligent defense systems. Meanwhile, government IT providers (e.g., SAIC, ManTech and Kratos), not wanting to cede ground, are pursuing acquisitions that add capabilities and expertise.

Foreign defense players (e.g., QinetiQ, Ultra Electronics, Cobham and Finmeccanica) have also been active as they seek access to the world’s largest defense market. The U.S. government, through the Committee on Foreign Investment in the United States (CFIUS), has become more comfortable permitting sales to non-U.S. entities, with information classified as “top secret” or above being controlled through proxy agreements/ voting trusts.

Organizational conflict of interest (OCI) legislation within the Weapon Systems Acquisition Reform Act of 2009 is also affecting transaction activity of prime defense contractors (primes). Primes are likely auditing existing systems engineering and technical assistance (SETA) contracts to assess potential conflicts with large acquisition programs. SETA opportunities therefore may shift back to traditional government IT providers, as primes withdraw from areas that pose potential conflicts. Northrop’s recent divestiture of its TASC unit, a provider of advisory services to the DoD, is a good example of a sale resulting from the new OCI legislation.

A decade of acquisition and change

The M&A landscape within defense IT has changed significantly over the last decade. In the late 1990s and early 2000s, serial roll-ups consolidated the fragmented government IT sector and created businesses of scale. Growth was fueled by the government’s transition toward outsourcing government jobs, combined with the technology bubble, Y2K preparation and abundant IPO capital.

Prime defense contractors largely remained on the sidelines, making up less than 10% of buyers. In recent years, primes have accounted for around one-third of transactions, as defense IT has become increasingly central to national security.

Private company valuations within defense IT vary considerably according to company-specific factors relating to technology and expertise, contracts and customers, and growth and profitability. By way of illustration, smaller privately held companies (transaction value less than $50 million) trade at a median of 1.0x revenues; the top valuation quartile sells for more than 1.5x revenues, while the bottom quartile changes hands at less than 0.4x revenues. Buyers pay a premium for proprietary products/processes, full and open contracts, and significant future growth.

Unmanned vehicles take flight

(click to view full)

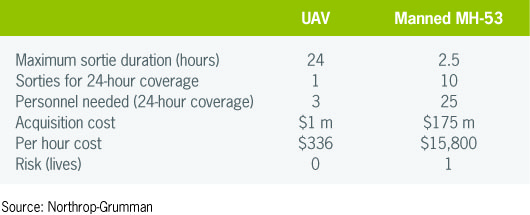

Unmanned aerial vehicles (UAVs) continue to be a focus of M&A activity, with 21 deals relating to UAVs (aircraft, components or electronics) occurring in the past four years.

UAVs have seen widespread adoption and are a major focus in the 2010 QDR, as they eliminate risk to humans, are cost-effective to procure and operate, have greater endurance and, consequently, gather significantly more data than manned aircraft.

Demand for UAVs is growing, not only as a replacement for manned aircraft, but more significantly due to their ability to carry out missions, particularly reconnaissance, not previously undertaken. Their very availability effectively creates demand and, as such, it is not surprising that in 2009 there were more UAV sorties than manned sorties by total number and significantly more by flying-hour. Demand for UAVs has increased six-fold since 2004 and is forecast to double again between 2010 and 2015. According to the 2010 proposed defense budget, UAVs will account for over one-third of planes purchased by the U.S. Air Force.

ISR drives growth in electronics

(click to view full)

Deal volume within the aerospace/defense electronics sector increased by 2% in 2009. Companies providing surveillance and other precision optical and imaging systems were especially hot targets, as strategic buyers sought to strengthen their capabilities in the high-growth tactical intelligence, surveillance and reconnaissance (ISR) market. Vision systems, such as night vision goggles, range finders and thermal weapon sights, have been increasingly in demand, with a marriage of technological advances and the rise in door-to-door combat operations.

Large firms within defense technology, prime defense and government IT have actively been acquiring businesses funded under the federal government’s Small Businesses Innovation Research (SBIR) program, as they seek to acquire cutting- edge products and technology. Over one-quarter (175) of SBIR businesses with 35 or more employees receiving Phase II prototype development awards have been purchased over the past 10 years with L-3, Lockheed, BAE, General Dynamics, Northrop and QinetiQ being particularly acquisitive. Acquired SBIR companies can be broadly characterized by activity as:

* 45% involved in electronics and electrical components, particularly communications, surveillance and optical equipment;

* 30% involved in software for IT security, command and control, and cyber security; and

* 20% involved in components and materials for aerospace, naval, and UAV applications.

Ian Cookson leads the Aerospace and Defense Group of Grant Thornton Corporate Finance LLC in the United States, where he advises on M&A transactions for clients ranging from leading multinationals to privately held companies. For further discussions and lists of defense IT and A&D electronics transactions, phone area code six one seven, 848 dash 4982. Or email Ian dot Cookson at gt dot com.

Additional Readings

* DID (July 21/10) – Lessons from the Automotive Supply Chain: Surviving a Downturn. By Vince Pavlak.

* DID (July 11/10) – “Grant Thorton: US Defense Budget Outlook for 2011 and Beyond. By Vice-Adm. Crenshaw (ret.)

* DID (March 15/09) – Grant Thornton on US Aerospace Component M&A, 2008