Guest Article by Christina Balis, Avascent

This is a pivotal year for the Polish defense market. Russia’s actions in Ukraine have underscored the urgency of Poland’s $44 billion military modernization program, and accelerated planned purchases. Critical defense procurement decisions will be made in 2014, testing the government’s ability to successfully manage big international tenders that pit Americans against Europeans. This year will also see the implementation of the country’s highly ambitious plans to consolidate most of its domestic industrial base under one roof, with significant implications for foreign suppliers seeking industrial arrangements with local partners.

Naturally, foreign companies are eager to secure a share in Europe’s most promising defense market. To compete effectively, defense primes and their subcontractors need to understand the financial, industrial, and political landscape they face in Poland.

The Polish Opportunity

(click to view full)

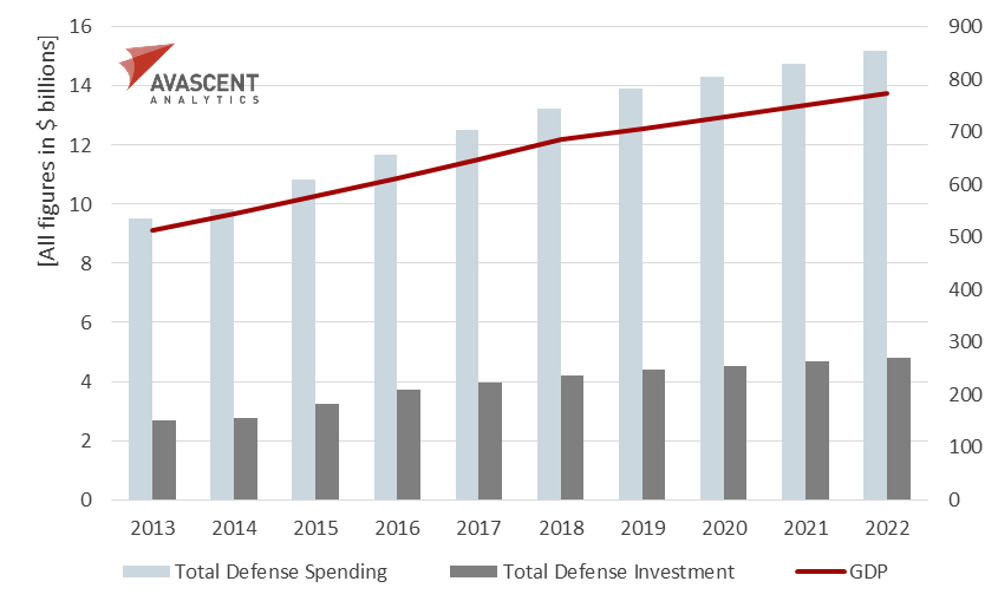

At PLN 32 billion ($10 billion), Poland’s current defense budget is a fraction of Europe’s biggest spenders, but outlays are set to grow faster than any other country on the continent. Poland is on a path to overtake Spain and the Netherlands in total defense spending in the next 2 years. (In terms of pure defense investment, Poland already ranks 5th behind the UK, France, Germany, and Italy). Poland has committed to maintaining its defense budget at no less than 1.95% of the previous year’s GDP, a level currently met or exceeded by only 2 other European NATO members: the UK, and Greece.

That GDP continues to grow. The Polish economy, now the 6th largest in the EU, is also among the healthiest. It survived the global financial crisis and Eurozone recession remarkably well, and GDP is estimated to grow in real terms by 3.4% next year, compared to the EU’s 2% average. Poland’s long-term growth is underwritten by the country’s growing exports, strong foreign investment, and some EUR 106 billion in EU funds to be allocated in 2014-2020.

Poland’s TMP is highly ambitious both in scale and in scope. Valued at about PLN 131.2 billion ($44 billion), the ten-year program touches on every aspect of the country’s defense apparatus. Weapons procurement accounts for 70% of the total, comprising 14 different operational areas.

At the beginning of the country’s 2013-2022 Technical Modernization Program (TMP), Avascent estimates that the Polish defense market was worth some $2.7 billion. This annual figure, which comprises all defense investment and excludes spending on personnel and ongoing operations, is expected to grow to $4.8 billion by 2022. While the Ukraine crisis is unlikely to prompt any further boost for Polish defense spending, it should ensure the planned modernization is kept largely on schedule, and even hastened in select capability areas like attack helicopters.

In sum, the size of the opportunity combined with solid economic fundamentals and an enabling security environment, makes Poland one of the most attractive defense markets for firms looking to improve their top line with exports.

Polish Partners: The Industrial Angle

(click to view full)

Poland’s military modernization program is closely intertwined with the government’s bold plans for developing its defense industrial base. While open competition and formal tenders have become the standard in large-scale contracts, industrial participation has become a key criterion in the selection of foreign bidders.

All government procurements must comply with the country’s Public Procurement Law (PPL) as amended in 2013 and consistent with EU regulations. Where procurement is exempt from the PPL because of national security interests, offsets under the New Offset Act of June 2014 may apply (formally the EU bans all types of offsets because they contravene internal market rules). In reality, however, industrial participation known as “Polonization” has supplanted offset rules, with 25% often seen as the minimum threshold for Polish participation in the production process – be it in the form of significant subcontractor work, local footprint, or working through a local partner.

In the land systems sector, Polish industry typically takes the lead, sometimes working under license (e.g., the Rosomak APC, produced by WZM under license from Finland’s Patria) or in close collaboration with a foreign supplier (e.g., PHO and BAE Systems partnering on the development of a tracked platform based on the Swedish CV90 IFV design). Polish industry was upset when the government opted to buy 119 Leopard 2A5 tanks from the German army, instead of paying for a new-design Polish option, but Germany’s extremely low price was an offer they could not refuse. In the air, missile and naval domains, by necessity, foreign primes remain in the lead but local industrial content can be the determining factor in procurement selections.

Polonization is designed to strengthen the country’s defense industrial capabilities and key competencies in areas consistent with the TMP. This is not unlike the implicit or explicit policies of other European countries. The UK’s 2005 Defense Industrial Strategy identified 12 sectors where the government seeks to retain sovereignty and “operational independence.” However, contrary to the UK and other countries in Europe, Poland’s defense industrial base remains both fragmented and largely inefficient.

The pending far-reaching consolidation of the Polish defense industry under PGZ (the Polish acronym for “Polish Armaments Group”) is intended to address these shortcomings – a move fraught with uncertainties for both local players and foreign partners.

Registered formally in late 2013, PGZ obtained control of 17 entities in May and is now entering the critical second stage of the consolidation process. By the end of the year, PGZ should see the transfer of shares from companies belonging to PHO, or Polish Defence Holding, the country’s largest defense company and itself the recent result of a merger of some 40 entities. PGZ will ultimately comprise at least 30 companies, previously controlled by the MND, the State Treasury and the Industrial Development Agency, a joint stock company owned by the Treasury and responsible for implementing state industrial policy. To be sure, greater scale will not make Polish industry more competitive overseas nor will integration automatically ensure improved efficiency at home. The integration of so many disparate state-run firms presents an organizational, and political, nightmare.

The greatest risk lies in the execution of such an ambitious industrial restructuring, even one based on a sound underlying strategy. Recent history makes this clear. The government’s previous plans to partially consolidate and privatize the defense sector (under its Strategy of Consolidation and Support of Development of Polish Defence Industry in 2007-2012) proved impractical within the original timeframe, and plans to merge Bumar (since renamed PHO) with Huta Stalowa Wola had to be scrapped. Why should setting up PGZ be any easier or more successful? It also remains to be seen how the transfer of PHO minority shares to PGZ will affect other companies, notably Gdynia-based radar company Radmor, controlled by Poland’s largest privately held group, WB Electronics.

The government’s evolving thinking on industrial consolidation has significant implications for foreign players and international partnerships. It is unclear how PGZ will operate as a whole, particularly given historical rivalries among some of its constituent elements, what degree of autonomy will be left to individual entities, or how consolidation of capabilities within the group and the creation of centers of competence across the broader industrial base will occur over time. Given the requirements for Polonization and industrial participation, foreign suppliers can ill afford ignoring these ongoing developments within the Polish defense industry. Even the most tactical pursuit, let alone long-term success, in the Polish defense market requires proper due diligence in the selection of partners and close monitoring of the government’s evolving defense industrial plans.

No Simple Choices: Purchases as Geo-Strategy

(click to view full)

For the past decade, Poland has thought about its future as a nation aligned with both America (through NATO) and Europe (through the EU). Yet Poland’s defense modernization may now force it to pick sides, in a sense, between American and European defense industrial partnerships. These industrial choices will force them to consider near-term jobs and investment, long-term opportunities that can help Poland maintain a strong national defense sector, and the uncertain quality of security guarantees on both sides of the Atlantic.

Poland sees the European strategic environment through a unique perspective. Historically, the scars of the 20th century linger. Geographically, it’s the largest border country in the eastern part of the EU. Vladimir Putin’s ambitions add urgency to Poland’s modernization plans, and indeed validated the country’s often-alleged “paranoia” about Russia. As Joseph Heller reminded us in Catch-22, just because you’re paranoid doesn’t mean they aren’t out to get you.

In that kind of environment, outside events and near-term decisions may have long-term consequences.

US responses to the crisis in Ukraine, including the dispatch of US F-16s to Poland shortly after Russia’s intervention in early March, and the $1 billion European Reassurance Initiative announced by President Barack Obama in early June, have been predictably faster and more forceful than Europe’s. That doesn’t change the revelations that senior Polish officials have lost a great deal of trust in the United States, but it may help.

(click to view full)

Meanwhile, the EU sanctions on Russia that took effect on August 1 are far more extensive than previous restrictions. On the other hand, it took the EU fully 5 months to reach this modest point, following Russia’s illegal annexation of Crimea, and events continue to unfold in the Ukraine. France’s dogged refusal to cancel delivery of the first of 2 Vladivostok Class amphibious assault ships sold to Russia (first delivery is expected in October) could ultimately harm French industry in Poland, despite strengthened bilateral ties over the past couple of years.

None of this eliminates the need to buy the best military capability, even if other considerations sometimes relegate it to one factor among many. Polish history doesn’t suggest a tremendous margin for error, and Poland’s terrain, geography, and plausible threats will make some platforms better than others at meeting the country’s needs.

In sum, Poland will have to juggle military capability requirements, industrial imperatives, and geo-strategic considerations as it seeks to complete 3 of the largest defense purchases under its modernization program in the coming 18 months. The bad news is that those considerations sometimes work at cross-purposes.

Poland’s choices will be a complex balancing act. Part 2 will look at those 3 competitions, and the balancing acts associated with each.

Avascent is the leading strategy and management consulting firm advising clients in defense, security and government-driven industries. With a team of 100 full-time professionals located at its offices in Washington, DC, and Paris, France, and a worldwide network of regional and subject matter experts, Avascent has nearly 30 years of experience of assisting clients in the areas of strategic growth, value capture, and mergers and acquisitions. To speak to Business Development, contract Jay Korman. For further information about Avascent’s European operations, contact Christina Balis.

Additional Readings

* DID – Poland’s Balancing Act: A Briefing for the Defense Sector – Part 2. Follow-on to this article.

* DID – Alone, If Necessary: The Shield of Poland. Poland’s future 3-tiered air and missile defense system.

* DID – Quote the Raven: Poland’s Attack Helicopter Competition.

* DID – Turkey’s TUHP: $3.5b for 109 T-70 Helicopters – and More. Actually, the S-70i. Turkey has positioned themselves to be able to step into Poland’s prime industrial role for the type, if circumstances allow.

* DID – Poland’s New Advanced Jet Trainer: M-346 Wins. The win ended up being budget-driven, not capability-driven. Will that history repeat?

* DID – Poland to Extend, Improve Its FFG-7 Frigates. Well, one of them, anyway. And the improvements are limited.

* DID – Buy from the Pros: Poland Adds More German Tanks.

News & Views

* XX Committee (Oct 27/14) – Poland Prepares for Russian Invasion. Author is former intel; measures include recreation of the Home Army paramilitary force. High-level Polish assessments of the USA are chilling.

* Nowa Straegia (Sept 3/14) – Czy mozemy czuc sie bezpieczni? Translates as “can we feel safe”; details modernization plans and discusses major areas.

* DID (Sept 9/14) – Polish Defence Modernization: Between strategic intent and spending reality. Looks at a different aspect: asks if the TMP’s full $44 billion in funding will really be there, and what that might mean.

* Foreign Policy Association (Sept 18/13) – Beyond Air and Missile Defense: Modernization of the Polish Armed Forces.

* Polish MON (Sept 18/13) – Money for new military equipment guaranteed.

* DID (July 23/13) – German Submarines for Poland? The country’s submarine plans remain murky.

* DID (July 18/13) – Poland Expands Orders for Rosomak Wheeled IFVs. A variant of Patria’s AMV. They’ve also worked with Israel’s Elbit Systems to offer UAV integration.

* DID (Oct 2/12) – Polish Equipment Issues and Consequences. In August 2009, Polish Land Forces Commander Lt. Gen Waldemar Skrzypczak resigned, accusing defense bureaucrats in Warsaw of “serious incompetence” in procurement that was partly responsible for the deaths of Polish soldiers.

* DID (Sept 12/11) – Poland to Modernize 16 MiG-29s. But they seem to have chosen a very basic upgrade.